How to Take Control of Your Credit

A Beginner's Guide to Understanding and Improving Your Credit

Your credit history follows you throughout your life, for better or worse, shaping your financial well-being and impacting your access to credit. The higher your credit score, the easier it is to get an auto loan, mortgage, or credit card, and the lower your score the more you will pay in interest and the harder it is to get the credit you need. And your credit history can affect your ability to get a job or rent an apartment. Simply put, your credit matters.

Knowing where your score stands can help you make informed decisions when applying for a credit card, buying a home, getting a student loan, or as you work to build a better financial future. It is the first step toward taking control of your credit. Making sense of it all, the different scores, bureaus, and factors, can seem daunting and confusing - but it doesn’t have to be.

Below is a beginner’s guide to everything you need to know to navigate your credit - from the differences between credit scoring models to the factors that go into your score and the steps you can take to start working toward your credit goals today.

- Understanding Credit Scores and Reports

- Why Your Credit Score Matters

- What is a Good Credit Score?

- Factors that Affect Your Credit Score

- How to Improve Your Credit Score

- How to Freeze Your Credit

Understanding Credit Scores and Reports

There are three major credit bureaus in the United States - Equifax, TransUnion, and Experian. These bureaus collect data from tens of thousands of sources, from credit card companies and banks to collection agencies and businesses, to build a comprehensive profile of your credit history. Each bureau maintains its own report of your credit and the information on your report may vary from bureau to bureau. Your credit score is based on the information on your credit report.

Your credit report details your payment history, accounts, balances, and more. It is used to calculate your credit score, which lenders use to help decide whether or not to lend to you and at what interest rate. Your credit report, but not your score, may also be used by landlords or employers when you apply for rental housing or a job.

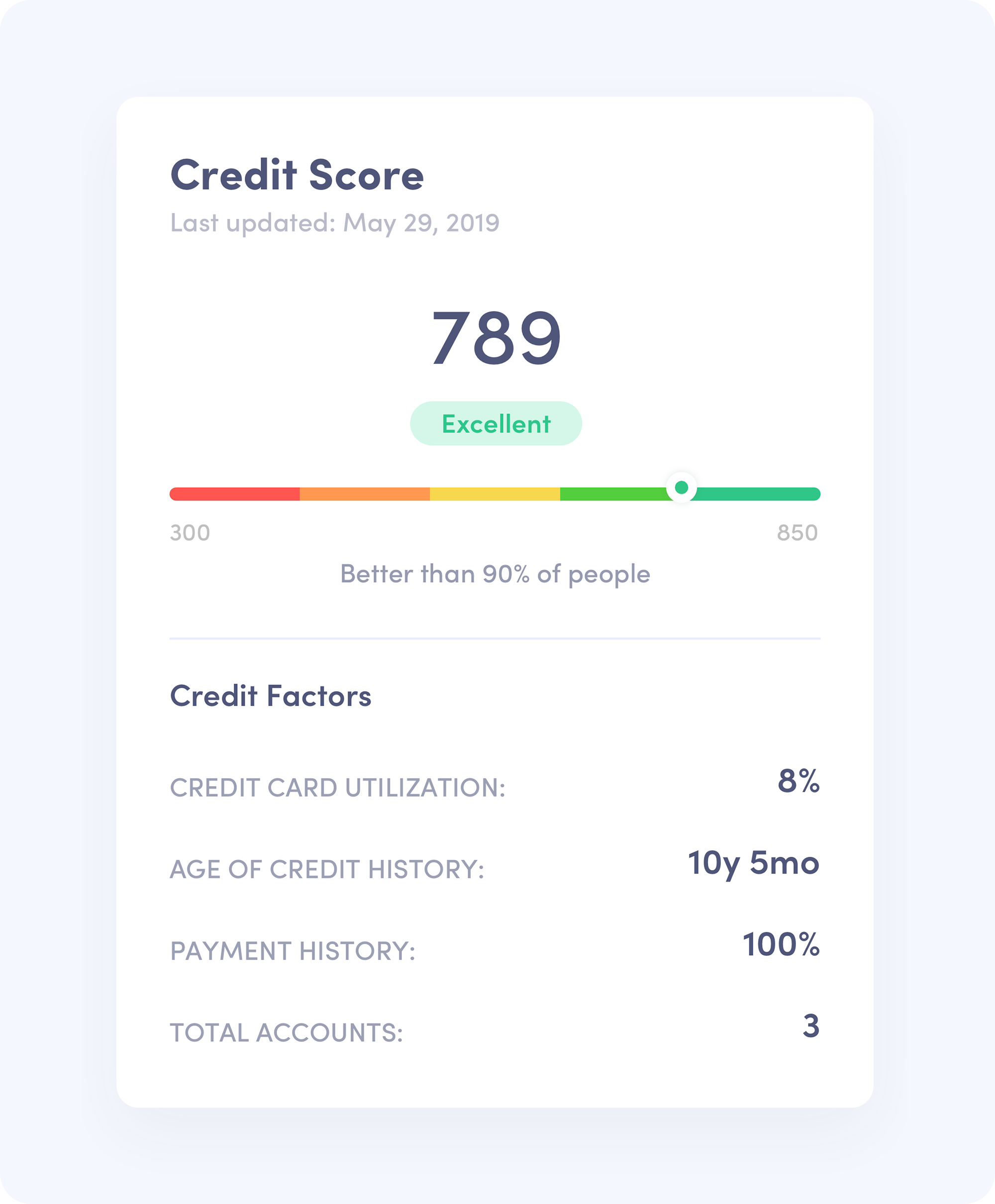

At its most basic, a credit score is a measure of your creditworthiness, i.e. your ability to repay. Your credit score is calculated from your credit report using a scoring model. The two most commonly used scoring models in the United States are FICO and VantageScore, both of which assign a credit score that ranges from 300 to 850. FICO, which has been around for decades, is used by more than 90% of lenders. VantageScore, a joint project between the three major credit reporting agencies, was developed more recently.

Your credit score will vary depending on which credit bureau your report comes from and which credit scoring model is used. For instance, your FICO score calculated using your Experian credit report will most likely differ from your VantageScore score calculated using your Equifax credit report. Each scoring model also has a number of versions, FICO 9 and VantageScore 4 are the most recent credit scoring models. Most free credit monitoring services use VantageScore to provide credit scores, while most lenders use FICO.

Why Your Credit Score Matters

Your credit score helps determine whether or not you get approved for a loan and the interest rate you will pay. A lower credit score could mean a smaller credit card line or higher interest rate on a mortgage. Or it could mean the difference between being able to buy a home or not.

Whether you are looking to buy a new car, open a new credit card, or buy a new home, your credit score matters. Managing your credit wisely and improving your score will make it easier to take out new loans when you need them and save you money in the long run. Even small differences in interest rates, especially on a mortgage or auto loan, can add up to thousands or tens of thousands of dollars in extra interest over the life a loan.

Beyond your score, employers and landlords may also ask to see your credit report, affecting your ability to get the right apartment or land a new job. Having a sterling report and a low debt-to-income ratio, a measure of your income relative to outstanding debt, are both important factors. One thing is for sure, credit has far reaching impacts.

What is a Good Credit Score?

While there is no set standard for what a good credit score is, there are some ranges for the two major credit scoring models that you can use as a good rule of thumb. Different lenders judge scores differently and what is a good or great score will also depend on what type of credit you are looking for. In general, the higher your score the more likely you are to get approved and the lower your interest rate.

Both FICO and VantageScore use a score range of 300 to 850. FICO and VantageScore use similar criteria to calculate a score but weigh factors differently. Use the ranges below to get a quick idea of where you stand.

VantageScore 3.0

- Excellent: 781-850

- Good: 720-780

- Fair: 658-719

- Poor: 601-657

- Very Poor: 300-600

FICO 8

FICO has two types of credit scores, base scores and industry-specific scores. For instance, mortgage lenders may use one scoring model while auto lenders use another. Some industry-specific scores range from 250-900 but the base score breaks down as follows.

- Excellent: 800-850

- Very Good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor: 300-579

Typically, VantageScore scores will be a bit higher than FICO scores. Before you apply for a loan, check with the lender to see which credit bureau and scoring model they use. A few points in either direction could determine whether or not you get approved.

So, what do these ranges actually mean when it comes to applying for credit? Knowing what range your credit score falls in can help you make smart financial decisions and avoid high interest rates and application denials.

300 to Low 600s: You’ll most likely have a hard time getting approved for a loan or credit card in this range. Typically, mortgage lenders define borrowers with FICO scores under 660 as sub-prime. To improve your score and build a positive payment history, you might want to look at a secured credit builder account or a secured credit card from one of the major credit card companies that allows you to put down a deposit in exchange for a credit line.

Mid 600s to Low 700s: You may be approved for an unsecured credit card but it will most likely come with a high interest rate or a less generous rewards program. You are also likely to be approved for a mortgage or auto loan but you will probably pay a higher interest rate. It’s important to note that your income, debt-to-income ratio, and any current delinquencies will impact what loans you are approved for.

Mid 700s and Above: If you’re in this range, you’re considered a prime borrower. You’ll likely be approved for most loans and offered the best interest rates and terms. A score in the mid 700s or above will give you the most options and flexibility in shopping around for the best rates. However, other factors such as your income, total debt, and any recent derogatory marks still play a role in approval.

Factors that Affect Your Credit Score

There are a few common factors that go into your credit score, even if they are weighted differently depending on the model used to calculate the score. Knowing where you stand and how these factors affect your score is important in improving your credit score.

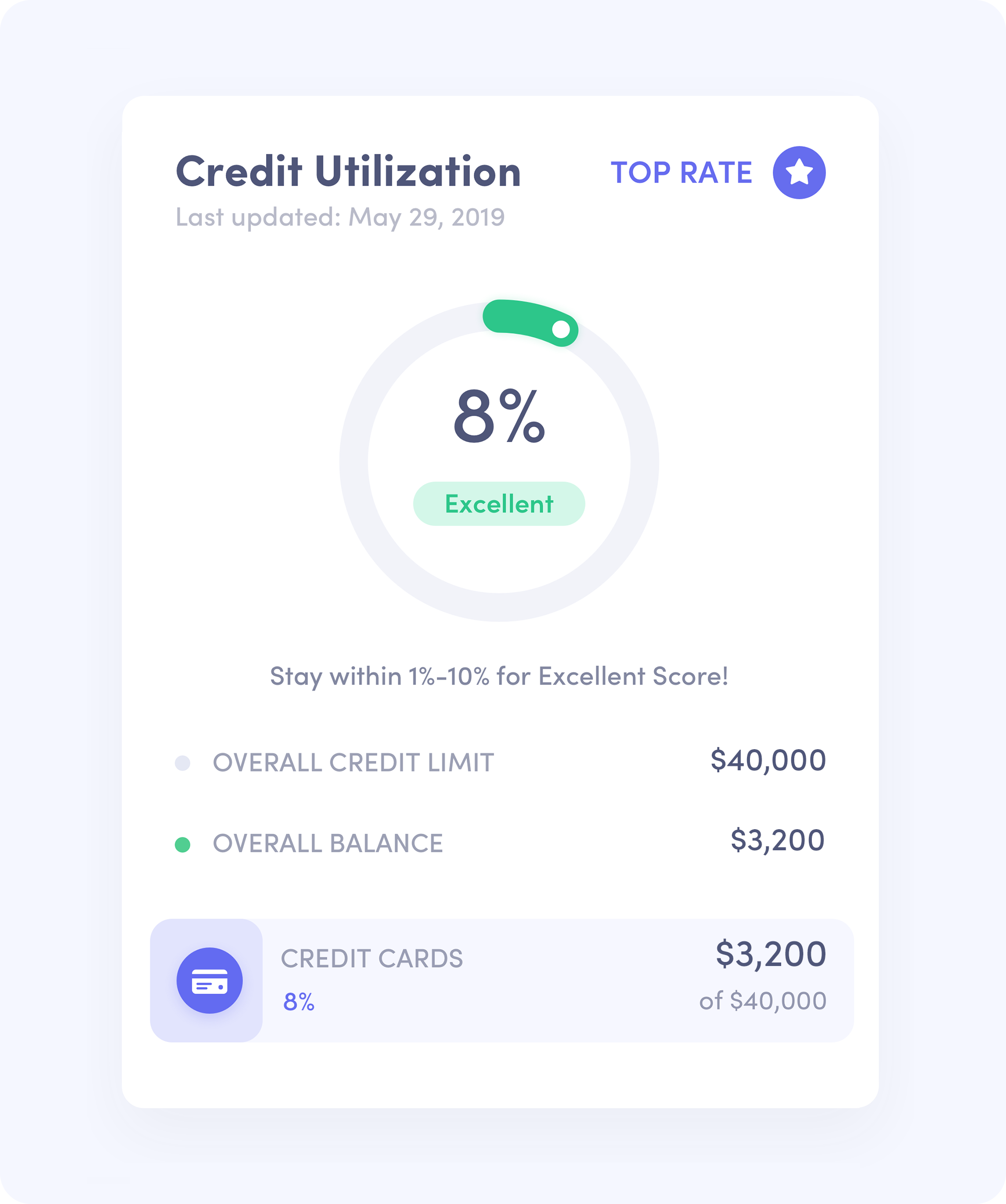

Credit Card Utilization (High Impact)

Credit card utilization is one of the most important factors in your credit score. It makes up about 30% of your FICO score and 20% of your VS3 score. Your credit card utilization, sometimes called revolving utilization, is determined by the total balance owed on your credit card accounts and your total credit line.

You can quickly calculate your utilization by dividing the total balance by total credit limit. For instance, if the total credit limit across your credit cards is $1000 and your current total balance is $500, your credit utilization would be 50%. A good rule of thumb is to keep your total credit utilization ratio below 30%.

- Excellent: Less than 10%

- Good: 10-29%

- Fair: 30-49%

- Poor: 50-100%

To help keep your utilization low, try to pay your credit card balances in full each month. By paying in full you will also avoid paying interest on your cards. If you can’t pay in full, pay down the balances across your cards so that you are using less than 30% of your total credit line. If you’re carrying large balances across your cards, you may also want to look into transferring your balances to a new one.

If you really want to maximize your score, keep your utilization below 10% for the biggest boost.

Payment History (High Impact)

Your payment history makes up about 35% of your FICO score and 40% of your VS3 score, so paying on time each month is the easiest way to keep your score up. Your payment history is made up of the payments on all of your accounts - mortgages, auto loans, credit cards, student loans, and personal loans. Reliably paying off your loans over time is the surest path to growing your score.

The more missed payments, the lower your score, so make sure you are at least making minimum payments each month. A solid payment history takes time to build up, so don’t get down if you’re just starting out. Building a long history of on-time payments is the best way to build a good credit score.

If you have trouble remembering monthly payments, try putting monthly reminders on your calendar to make sure you never miss a payment. If you are struggling to make payments, contact your lenders to see if you can adjust or set up payment arrangements based on your circumstances.

Derogatory Marks (High Impact)

If you fall far enough behind on payments on an account, it may go to collections. Collections show up on your credit report as derogatory marks and can stay on your report for up to 7 years. Other types of derogatory marks include foreclosure, repossession, and bankruptcy.

Here are some common derogatory marks and how long they can stay on your credit report:

- Account Charge-Off: 7 years

- Repossession: 7 years

- Collections: 7 years

- Student Loan Default: 7 years

- Bankruptcy: 10 years for Chapter 7

- Foreclosure: 7 years

The best thing to do is try to avoid derogatory marks in the first place. Make all your payments on time. If you aren’t able to make payments, contact the lender to see if you can come up with a payment arrangement so that your account isn’t charged off or sent to collections. It’s important to note that collections can come from non-financial accounts. For instance, unpaid cable, utility, or medical bills can become collection accounts that show up on your credit report.

Length of Credit History and Mix (Medium Impact)

The length of your credit history is determined by how long you’ve had your open accounts. The older the better. Again, building a long credit history takes time and patience, which is why it is important to focus on the long term sustainability of your credit and steadily improving your score over time. For this reason, it is also best to space out opening new accounts. Too many new accounts all at once will bring down the average age of your accounts.

Keeping your accounts open and in good standing is the most important thing you can do overall. Make sure to regularly use your credit cards so that they aren’t closed due to inactivity and don’t close accounts just because you haven’t used them in awhile, unless they have large annual fees. If you have a card with a high annual fee, check with your credit card company to see if they will waive it before closing the account.

Another factor to keep in mind is a healthy mix of different types of credit. This shows lenders that you are able to manage various types of credit well. You generally want to avoid having too many accounts of one type of credit, such as only credit cards.

Hard Inquiries (Low Impact)

When you apply for credit, the lender will often pull your credit report and score from a bureau, often referred to as a “credit check”. There are two types of inquiries, soft and hard pulls. A hard pull will show up on your credit report as a hard inquiry, while a soft pull won’t affect your credit. Hard inquiries are low impact and won’t hurt your score much unless you rack up a lot of them. However, you should try to keep the number of inquiries down and avoid applying for credit that you aren’t likely to qualify for.

A high number of inquiries in a short period of time signals to lenders that you may be experiencing financial hardship and make you more of a credit risk. There are some exceptions to this rule. When shopping around for the best auto loan, if the inquiries occur within a certain time period, usually 14 days, they will be counted as a single inquiry. This allows you to shop for a car without negatively impacting your credit. If you’re looking to buy a home, inquiries made by mortgage lenders and brokers in a 45 day window are also counted as one.

Hard inquiries typically stay on your credit report for up to two years but their impact on your score will begin to fade after a year. You can also check for pre-qualified credit card offers to increase the likelihood of approval so that you don’t have to apply for multiple cards in order to get approved, which could lead to multiple inquiries.

How to Improve Your Credit Score

Building a great credit score can take years but there are some steps you can take to start improving today. Don’t aim for a perfect score, which is all but impossible, but rather aim to slowly and steadily improve your credit score over time. By following some basic rules of thumb, you can start to make improvements and set yourself on a sustainable course that will make managing your score less stressful and help you achieve your goals.

Follow the steps below to get started:

1. Check Your Credit Reports Regularly

The first step in improving your credit score is knowing where you stand. Check your score regularly to track your progress. Checking your reports can also help you identify inaccuracies or potential identity fraud. Once you have a good idea of what’s on your report and what range your score currently falls in, you’ll start to get the feel for how changes to your report, such as a lower utilization ratio or new account, affect your score. Then you can start setting some credit goals.

2. Maintain a Low Credit Utilization Ratio

The biggest boost you can get immediately is to lower your credit utilization. If your balances are high, try to pay each one down as much as possible to bring your utilization down below 30%. For the biggest gains, aim for less than 10%. Another benefit of keeping utilization down is that it will help you avoid carrying balances from one month to another and thus reduce interest.

To help make sure you are hitting your target utilization, check your credit report to see when your credit card issuer reports your monthly balance. Most cards report your balance on the statement cut date. Then, make sure to pay the balance on each card before the report date. This will keep your balances as low as possible.

3. Pay Your Bills On Time

This is the most important thing you can do. Pay your bills on time every month. That means paying the bill for each one of your accounts on time, and if you can’t pay your credit card balances in full each month then make sure you at least make the minimum payment by the due date. If you have a history of late payments, there is never a better time to get things on track than right now.

This also goes for all bills, including utility, mobile, cable, and medical bills, so that you avoid any accounts going to collections. If you have a hard time remembering to pay your bills, set up reminders on your calendar or use a reminder app to send notifications a day or two before each bill is due. Staying on top of payments will pay off in the long run.

4. Don’t Close Old Credit Cards

It may sound counterintuitive, but don’t close old credit cards even if you no longer use them. Keeping open credit card accounts will help keep your total number of accounts up and increase the length of your credit history. If you have to close a card, close the one you’ve opened most recently. If you have an old card that you no longer use but still charges an annual fee, call the issuer and see if you can get the annual fee waived.

5. Set Realistic Credit Goals

At the end of the day, your credit score is a tool to help you build a healthy financial future and achieve your goals in life, whether that is to own a home, go to school, or have a variety of financial options should you ever need them. Setting realistic and sustainable credit goals now will help you gauge your progress and steadily build your credit so that you will be ready in the future. Don’t take on unnecessary debt just to pad your score or overextend yourself just to meet some arbitrary target score. Make your credit work for you. Focus on what it is you want and what it will take for you to get there.

How to Freeze Your Credit

One final thing that you should know how to do is how to freeze your credit. This is especially important in the event you suspect you’ve been a victim of identity theft. Freezing your credit is one of the most effective ways of reducing the risk of identity fraud and will help prevent fraudsters from opening up new financial accounts or lines of credit in your name.

Freezing your credit will not freeze your score. It will simply prevent new accounts from being opened under your name. Current accounts, payments, and balances will continue to update while your credit is frozen.

To freeze your credit you will need to make a credit freeze request directly with each of the three main credit bureaus - Experian, TransUnion, and Equifax. As of September 21, 2018, credit freezes with the three main bureaus are free for all consumers.

When making your request, you will be asked for your name, address, date of birth, and Social Security number, along with questions to verify your identity. Once your freeze has been processed you will be given a Personal Identification Number (PIN) that can be used to thaw or unfreeze your credit in the future.

- Freeze your credit with Equifax by clicking here or calling 1-800-685-1111

- Freeze your credit with Experian by clicking here or calling 1-888-397-3742

- Freeze your credit with TransUnion by clicking here or calling 1-888-909-8872

Once credit freezes are in place, you can use your PIN to temporarily thaw or unfreeze your credit if a business or lender needs to check your credit, for example, when applying for a credit card, auto loan, or mortgage, by contacting the bureaus directly.

Learn How to Protect Your Identity

Credit is integral to your identity and so is protecting it. For information on what you can do to safeguard your data and protect yourself online, check out our in-depth security and privacy guides:

- How to Protect Your Privacy Online

- How to Protect Your Phone from Being Hacked

- How to Protect Your Identity

- The Ultimate Guide to Data Breaches

Want to Learn More About Bloom?

- Bloom Radar: A Guide to Data Breach Monitoring

- BloomID: A Guide to Your Secure Identity

- How Bloom Keeps Your Data Secure

Bloom: Take Back Control of Your Credit

At Bloom, we are giving you the tools to take back control of your data. No more centralized data storage. No more selling off your data to the highest bidder. No more risking identity theft. Bloom enables you to own, control, and protect your data using the latest advancements in blockchain technology.

With Bloom:

- You own your data

- You control access to your data

- You decide when you share your data and who you share it with

It’s time to take back control of your data and unlock the power of a secure, reusable identity today. Download the Bloom mobile app to build a cryptographically secure identity and get free data breach alerts with Radar!